How Much Life Insurance Coverage Should I Have to Support My Family?

They say there are two things in life you can never run from: death and taxes.

A recent study by the Life Insurance Association of Singapore (LIA) found that the average working adult in Singapore has a S$170,000 life protection gap, or roughly 2.1 times the average annual income. But what does this mean for you, and how can you ensure that your dependents and loved ones are adequately covered in the event of your death?

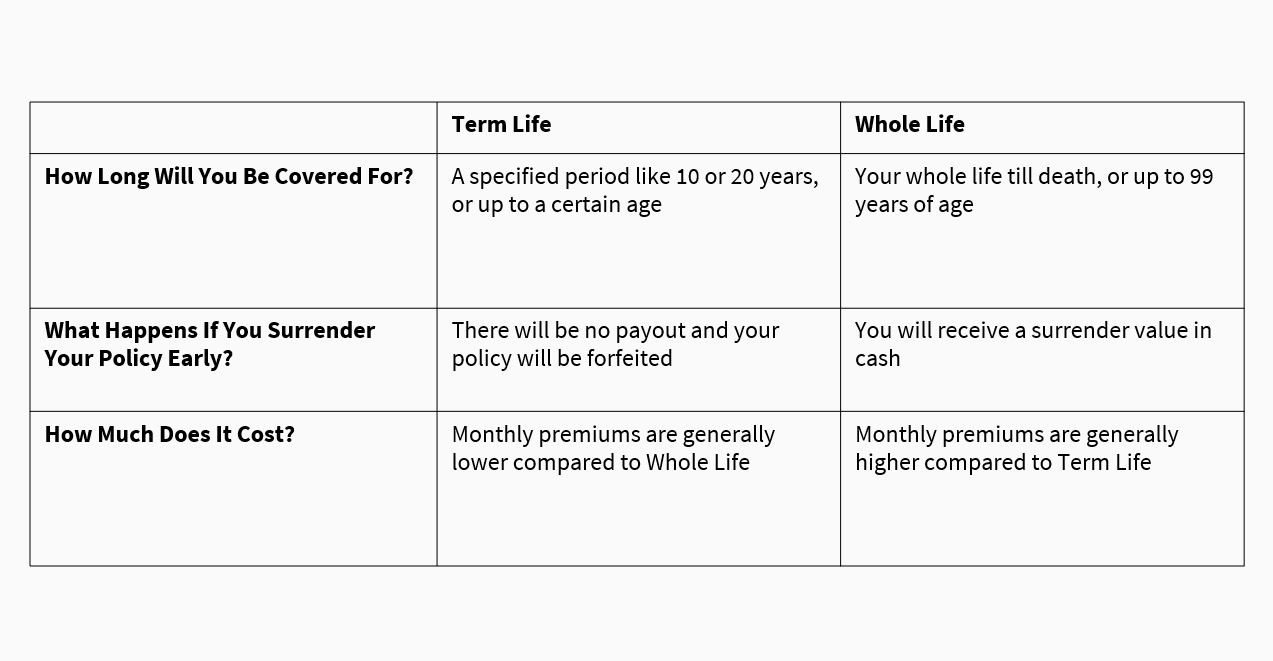

Whole Life and Term Life Insurance Plans

While many insurance plans provide some payout in the event of death, there are generally two types of life insurance policies available in Singapore: Term Life and Whole Life insurance. Here are the main differences.

Term Life plans tend to be more affordable, but they expire once their term is up and there is no cash value should you decide to surrender your policy. You can choose to renew your policy once your term is up, but premiums increase as you get older. Nonetheless, Term Life plans are an affordable way to ensure that your loved ones and dependents receive financial protection against your death.

Whole Life plans have higher premiums, but come with a cash value when the policy matures or when it’s surrendered. This is why, should you decide to terminate your plan prematurely, you may still recover some of your policy’s value in cash. Whole Life plans also offer life-long coverage with limited payment terms – this means that you only have to pay premiums for a fixed number of years but will enjoy coverage up till death.

Regardless of which type of life plan you choose, be sure to consider the following factors when determining the right amount of coverage for you:

- Your annual household expenditure

- Any existing liabilities

- Other assets

How Do I Calculate How Much Life Insurance Coverage I Need?

The answer, according to LIA’s Protection Gap Study, takes into account a holistic view of your other assets and liabilities. Using the same principles, you can calculate your Life Insurance needs as:

Protection Needs - Resources Available = Ideal Life Insurance Coverage Amount

Protection Needs include:

- Funeral costs and any unpaid medical expenses

- Any outstanding debts, including personal and housing loans

- Ongoing expenses for dependents, such as children’s education needs, elderly parents’ needs, household expenses, and more

Resources Available covers:

- CPF and other savings accounts (cash and/or investment)

- Existing insurance coverage

- Any other assets such as property or real estate

Annual Household Expenditure

Think of life insurance as a means of income replacement. Calculate your family’s usual living expenses and consider how long they will need to be covered for if you were to die today.

For example, if you only need to cover expenses for your children until they are financially independent, how many years will that take? How many years will your elderly parents need your financial support, or how long will your spouse take to find a job?

Also consider if your death will cause additional expenses, such as the need to hire additional help for caregiving or childcare.

Existing Liabilities

Most importantly, do not neglect your outstanding debts, because these will be deducted from your estate (which includes your insurance coverage) upon your death. Do you have any outstanding personal loans, car loans, or mortgages that need paying off? Add these to your ‘Protection Needs’ bucket.

Also take into account your funeral costs, and include a buffer amount to deal with any unpaid medical costs that may arise from your death. The average funeral in Singapore costs anything from S$1,800 to S$8,400.

Here is the LIA life insurance calculator, which can help give you an idea of how much life insurance coverage you may need.

Other Assets

Your protection needs do not have to be funded by insurance alone – consider accumulating other assets to add to your estate, which includes your CPF accounts, investments and savings accounts, property and real estate holdings, and more.

And yes, your other insurance policies can also be considered part of your estate too, especially if they pay out upon death (e.g. Mortgage Insurance).

There is a popular sentiment amongst those who choose Term Life over Whole Life that a minimal amount should be spent on life insurance because you can save on the premiums and channel more into savings or investments.

This makes sense, but you should also consider how much you can realistically save versus how much in premiums you are paying to receive the same amount of coverage with life insurance. It’s also important to consider if you can continue to maintain coverage in your old age, which is when you may need life insurance the most.

Other Tips to Get the Most out of Your Life Insurance

Start early to enjoy lower premiums, and enhance your coverage with riders. For example, adding on a Critical Illness Benefit rider will allow you to receive an early payout should you be diagnosed with one of the major illnesses covered (i.e. you don’t necessarily have to wait till death to benefit from a life insurance policy).

There are also riders that allow you to waive future premiums should you be struck with a sudden disability or illness, so that you can continue to enjoy coverage even if you can no longer afford premiums. Riders are a great way for you to customise your life insurance coverage and find the best combo that fits your needs and budget.

With life insurance, starting small is better than not starting at all. If you have loved ones who count on you to provide for them, life insurance is fundamental to ensuring that they will continue to be cared for even after you’re gone. You can always choose to build and increase your coverage later on as your responsibilities and financial circumstances change.

Disclaimer:

This article is for general information only and does not take into account the specific investment objectives, financial situation or needs of any particular person. The views expressed herein do not necessarily reflect the views of AXA Insurance Pte Ltd and should not be construed as the provision of advice or making of any recommendation. There is no intention to distribute, or offer to sell, or solicit any offer to purchase any product. We recommend that you seek the advice of a qualified financial advisory professional before making any decision to purchase an insurance or investment product. Whilst we have taken reasonable care to ensure that all information provided was obtained from reliable sources and correct at time of publishing, information may become outdated and opinions may change. We are not liable for any loss that may result from the access or use of the information herein provided.

|

|

|

|